|

The conflict unfolding around the Strait of Hormuz is rapidly evolving beyond a conventional military confrontation.

What is emerging instead is something more consequential for global markets: an energy and logistics crisis centered on the Gulf’s infrastructure and maritime chokepoints.

The region sits at the heart of the global hydrocarbon system, and the escalation we are now seeing reveals how fragile that system can be when geopolitics intersects with physical supply chains.

Below are five structural realities shaping the conflict and its implications for energy and shipping markets.

1. Energy infrastructure has become a primary battlefield

One of the clearest signals from the conflict so far is that energy infrastructure is no longer a secondary target — it is central to the strategy.

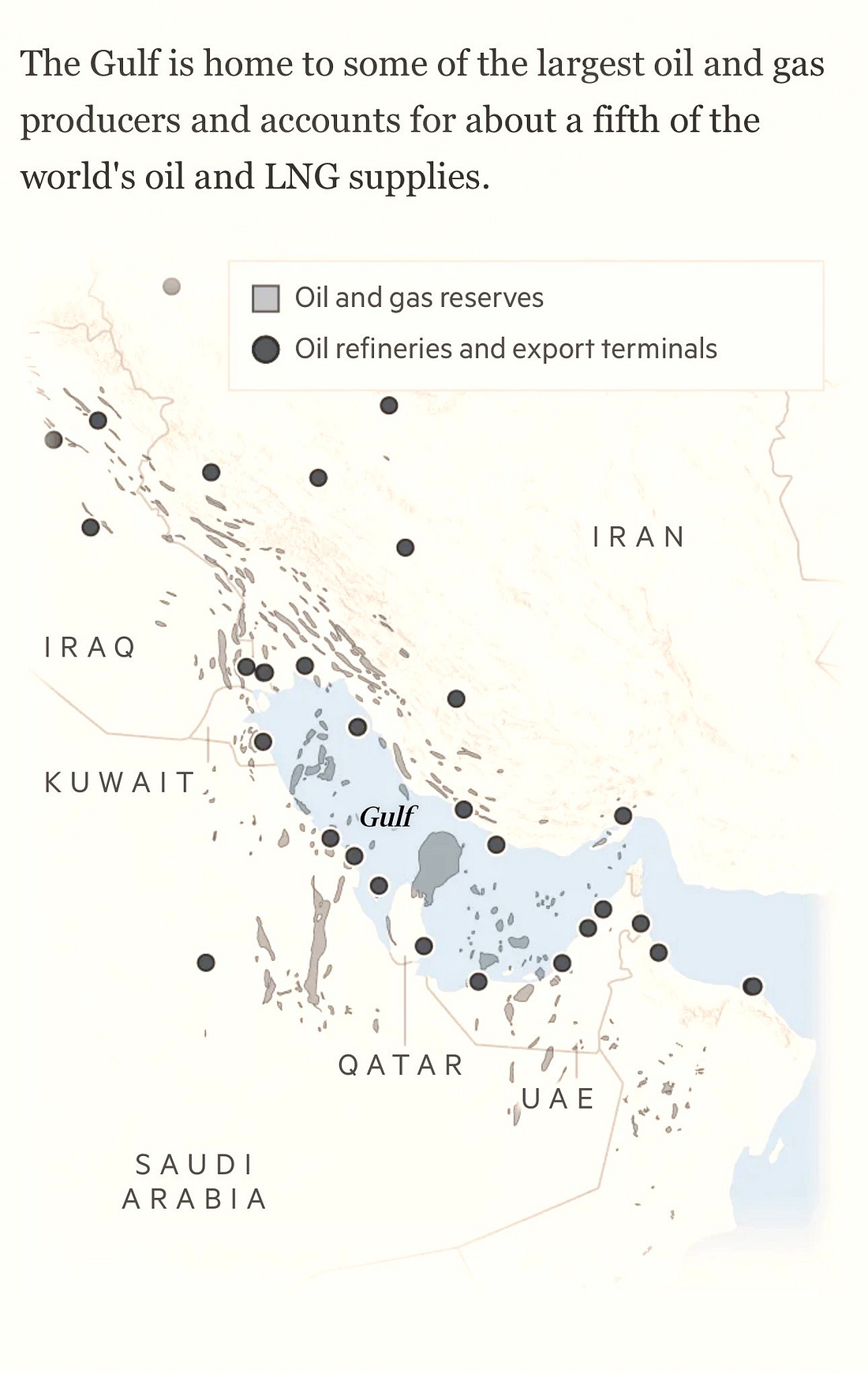

Facilities such as Saudi Arabia’s Ras Tanura Refinery and the massive LNG export complex at Ras Laffan Industrial City illustrate the scale of what is at stake.

These sites are not just industrial facilities; they are nodes in the global energy system.

The Gulf region accounts for roughly:

What makes this phase of the conflict particularly striking is how inexpensive the tools of disruption have become.

One of the clearest signals from the conflict so far is that energy infrastructure is no longer a secondary target — it is central to the strategy.

Facilities such as Saudi Arabia’s Ras Tanura Refinery and the massive LNG export complex at Ras Laffan Industrial City illustrate the scale of what is at stake.

These sites are not just industrial facilities; they are nodes in the global energy system.

The Gulf region accounts for roughly:

- ~20% of global oil supply

- ~20% of global LNG supply

What makes this phase of the conflict particularly striking is how inexpensive the tools of disruption have become.

Drone strikes and asymmetric attacks can threaten assets that took decades and hundreds of billions of dollars to build.

This creates a profound imbalance: cheap weapons targeting extremely expensive infrastructure.

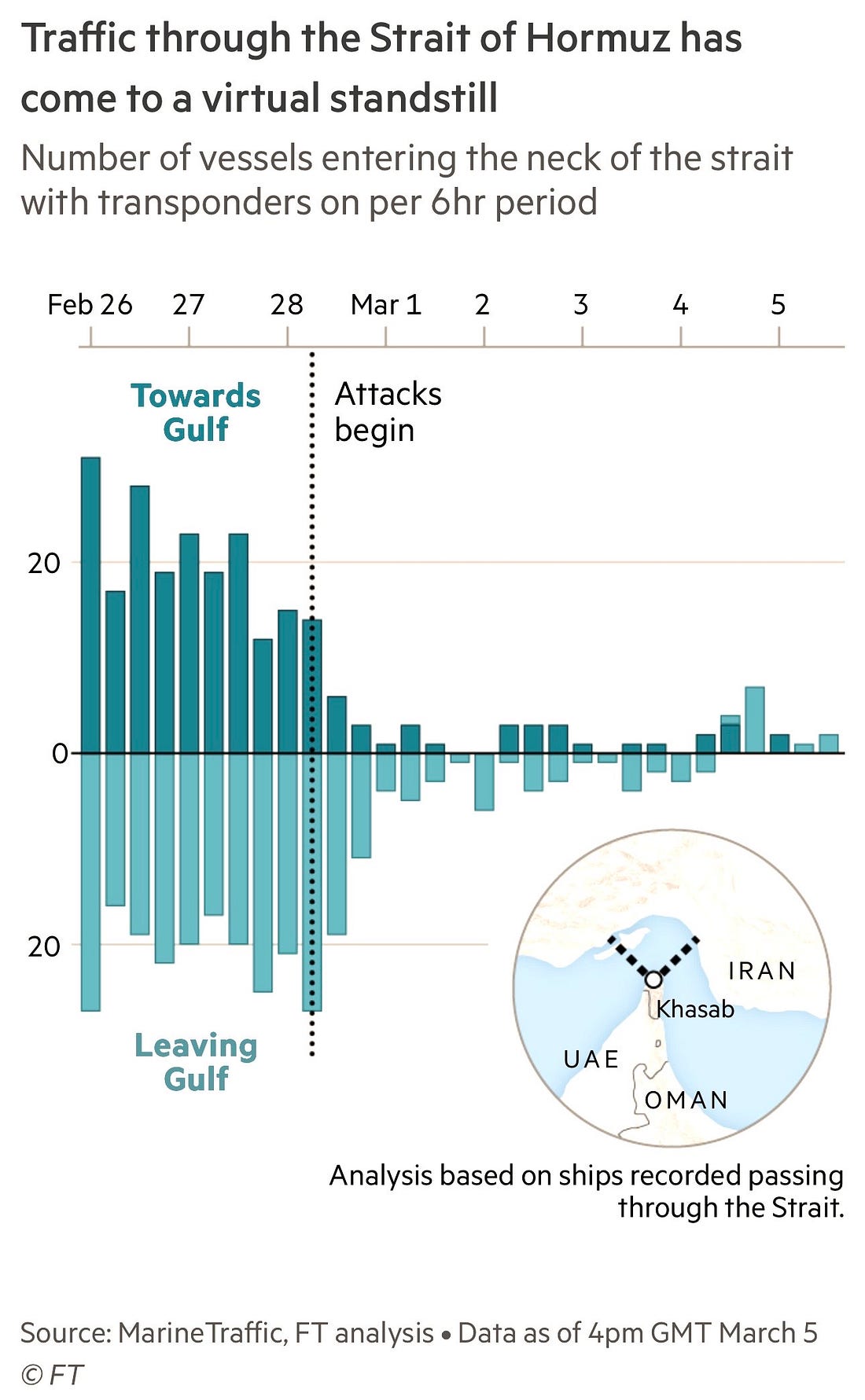

2. Shipping activity has effectively collapsed

The second front in this conflict is maritime.

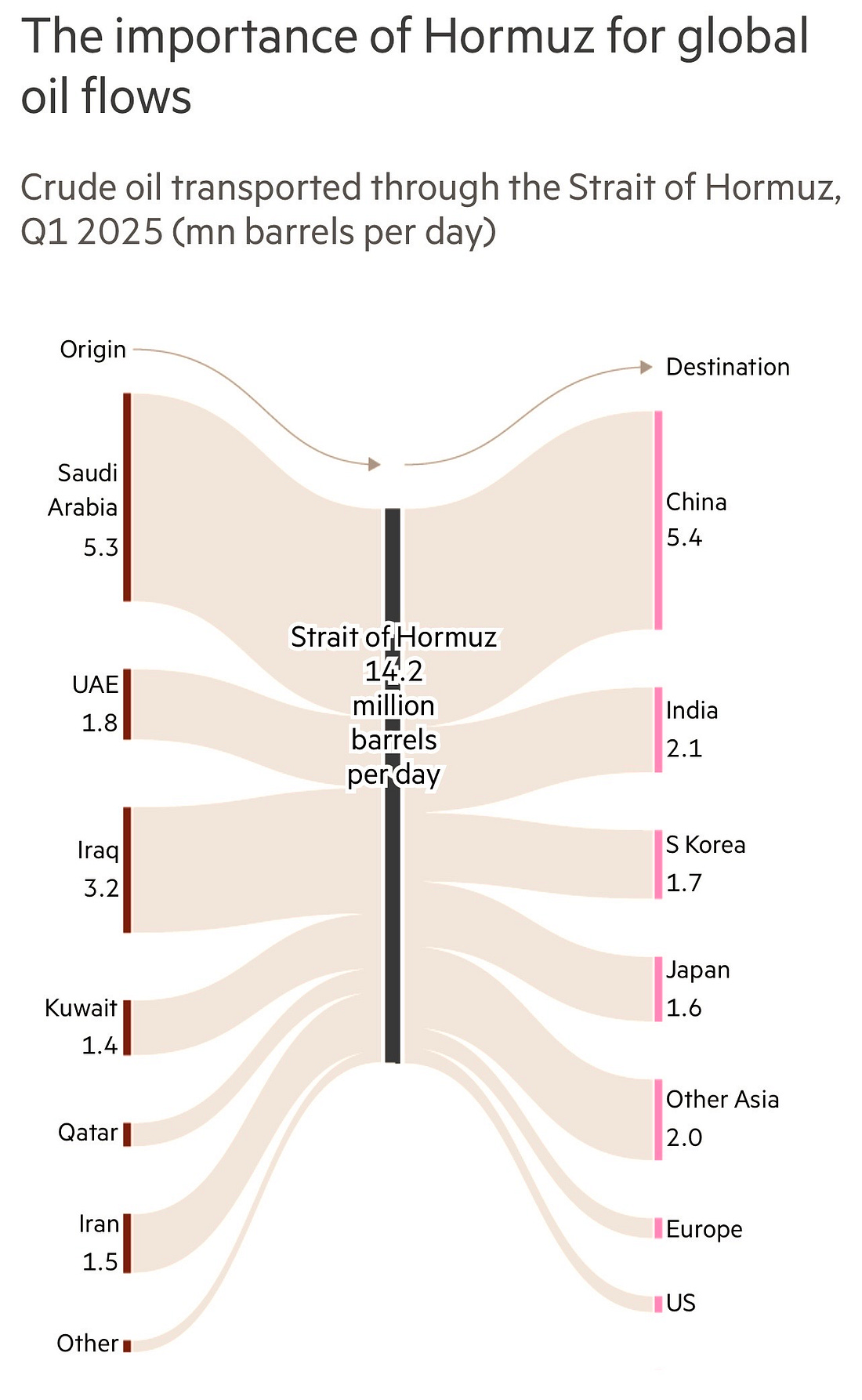

The Strait of Hormuz is one of the most critical shipping routes in the world. Roughly 20 million barrels of oil per daynormally transit this narrow waterway, alongside large volumes of LNG and other commodities.

But in recent days, commercial traffic has dropped sharply.

This creates a profound imbalance: cheap weapons targeting extremely expensive infrastructure.

2. Shipping activity has effectively collapsed

The second front in this conflict is maritime.

The Strait of Hormuz is one of the most critical shipping routes in the world. Roughly 20 million barrels of oil per daynormally transit this narrow waterway, alongside large volumes of LNG and other commodities.

But in recent days, commercial traffic has dropped sharply.

Some maritime intelligence reports suggest very few international vessels are crossing the Strait, apart from Iranian shipping.

This disruption extends far beyond hydrocarbons.

Several other commodity supply chains rely heavily on the Strait, including:

This disruption extends far beyond hydrocarbons.

Several other commodity supply chains rely heavily on the Strait, including:

- aluminium exports from the Gulf

- fertiliser feedstocks such as urea and sulphur

- petrochemicals

- other bulk commodities

War risk insurance premiums have surged, freight risk has increased dramatically, and many shipowners are reassessing whether the route is commercially viable under current conditions.

Iranian officials have further escalated tensions by warning that “not a single litre of oil” would leave the Gulf while attacks against Iran continue.

If enforced, such a strategy would effectively weaponize one of the world’s most important maritime chokepoints.

Iranian officials have further escalated tensions by warning that “not a single litre of oil” would leave the Gulf while attacks against Iran continue.

If enforced, such a strategy would effectively weaponize one of the world’s most important maritime chokepoints.

3. Storage and logistics constraints are creating a cascading crisis

A less visible but equally important dimension of the crisis is logistics bottlenecks within the producing countries themselves.

If exports are blocked, oil producers eventually face a simple physical constraint: they run out of storage capacity.

Tank farms fill quickly when production continues but tankers cannot load.

Once storage reaches its limits, producers have no choice but to shut in production.

Countries such as Iraq are particularly vulnerable to this dynamic because their storage capacity is limited relative to production levels.

Even where alternative export routes exist, they offer only partial relief.

Saudi Arabia can divert some crude through the East–West Pipeline, which transports oil to terminals on the Red Sea.

Countries such as Iraq are particularly vulnerable to this dynamic because their storage capacity is limited relative to production levels.

Even where alternative export routes exist, they offer only partial relief.

Saudi Arabia can divert some crude through the East–West Pipeline, which transports oil to terminals on the Red Sea.

The UAE has a similar bypass route through the Habshan–Fujairah Pipeline, allowing exports to reach the Gulf of Oman.

But these pipelines cannot replace the full capacity of the Strait.

But these pipelines cannot replace the full capacity of the Strait.

At best, they allow a fraction of normal export volumesto continue moving.

The result is a cascading supply problem: once exports slow, production reductions often follow.

4. Kharg Island is the strategic wildcard

Amid all the escalation, one location remains conspicuously untouched: Kharg Island Oil Terminal.

The result is a cascading supply problem: once exports slow, production reductions often follow.

4. Kharg Island is the strategic wildcard

Amid all the escalation, one location remains conspicuously untouched: Kharg Island Oil Terminal.

This small island handles around 90% of Iran’s crude exports and is one of the most strategically sensitive pieces of energy infrastructure in the region.

So far, the United States and Israel appear to have deliberately avoided targeting it.

The reason is straightforward: striking Kharg would likely trigger a far broader escalation.

Such an attack could provoke:

As long as it remains untouched, there is still some containment in the conflict.

So far, the United States and Israel appear to have deliberately avoided targeting it.

The reason is straightforward: striking Kharg would likely trigger a far broader escalation.

Such an attack could provoke:

- retaliatory strikes on Gulf energy infrastructure

- a severe disruption to regional oil exports

- a significant shock to global energy markets

As long as it remains untouched, there is still some containment in the conflict.

But if that line were crossed, the consequences for global energy markets could be profound.

5. The global energy system is structurally fragile

Taken together, these developments highlight a deeper structural reality.

The global energy system depends on a small number of highly concentrated infrastructure hubs and maritime chokepoints.

When those assets become exposed to geopolitical conflict, the system can be destabilized far more easily than many market participants assume.

Low-cost asymmetric warfare — whether drones, sabotage, or maritime disruption — now has the potential to:

Taken together, these developments highlight a deeper structural reality.

The global energy system depends on a small number of highly concentrated infrastructure hubs and maritime chokepoints.

When those assets become exposed to geopolitical conflict, the system can be destabilized far more easily than many market participants assume.

Low-cost asymmetric warfare — whether drones, sabotage, or maritime disruption — now has the potential to:

- damage critical infrastructure

- halt shipping routes

- destabilize commodity flows

- move global prices

It is also a stress test for the architecture of the global energy and shipping system.

And the results so far suggest that architecture may be far more fragile than markets once believed.

And the results so far suggest that architecture may be far more fragile than markets once believed.

Links :

No comments:

Post a Comment